The last eighteen months in small business M&A have been challenging to say the least. From March 2022 to January 2024, the federal reserve hiked interest rates a total of 11 times in an effort to curb rapid inflation and avoid a second recession in four years. This dramatic increase in rates and ultimately the cost of capital caused M&A activity across the world to come to a screeching halt. Based on data from CIBC & Baird, US lower middle market deal volume in 2023 declined by 26% year-over-year and was down 46% from 2021 peak levels. However, after a sluggish start to 2024, there might be some good news on the horizon with positive inflation readings from May and rumors of a possible rate cut in 2024.

Inflation Update

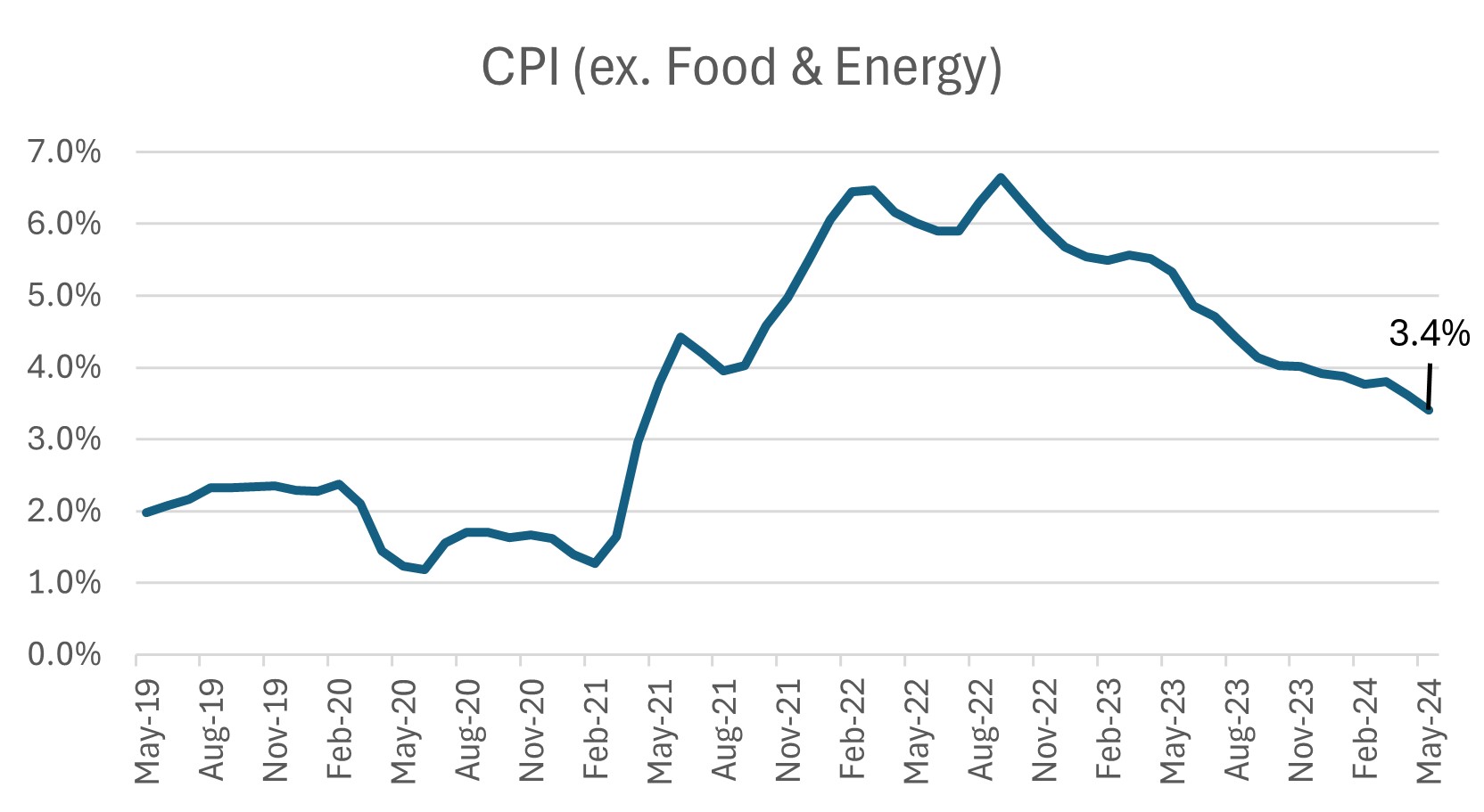

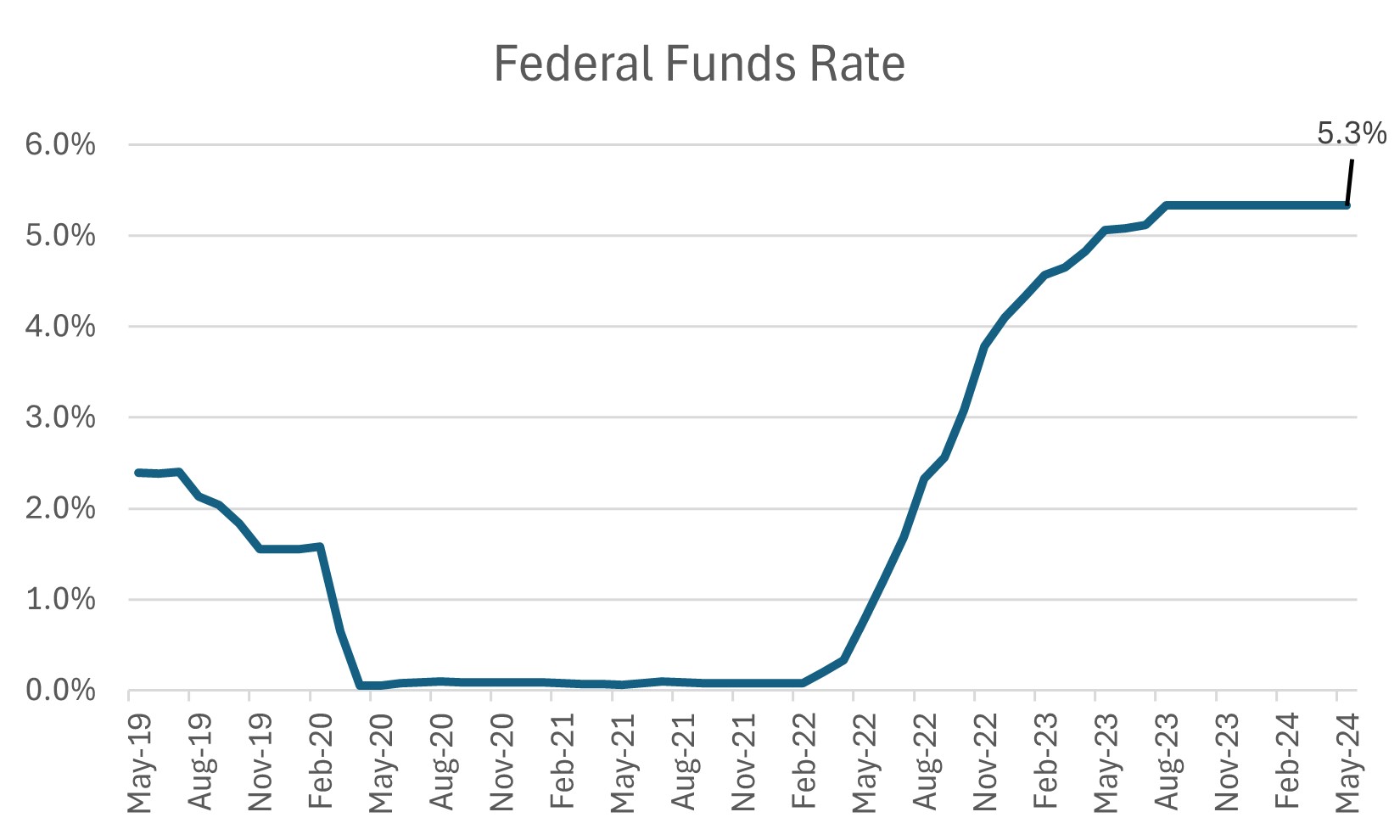

The Labor Department reported that the consumer-price index (measure of goods and service costs across the economy) was essentially flat from April. Based on the chart below, core prices (which exclude food and energy) rose 3.4% in May. Relatedly, core prices posted their lowest gain since April 2021. The May reading has largely come in below expectations and is described as encouraging. However, Fed Chair Powell has reiterated that the fight is not over. For now, Federal Reserve officials are estimating that there will finally be an interest rate cut in the second half of this year. Currently, the Fed is holding its benchmark rate steady, in the range between 5.25% and 5.5%.

Source: St. Louis Fed

Source: St. Louis Fed

Have valuations recovered?

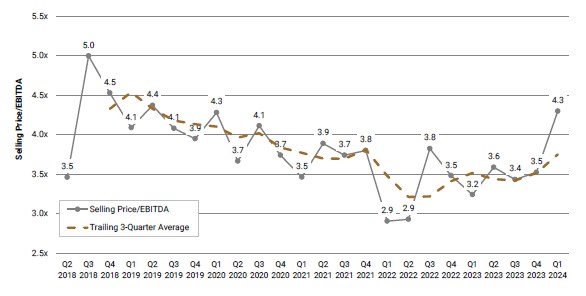

After a choppy end to 2023, exit multiples have shown resilience in the first quarter of 2024. According to data from DealStats, Q1 2024 sales price to EBITDA multiples for private companies rose to an average of 4.3x earnings from 3.5x in Q4 2023. Q1 2024 gains represent a year-over-year increase of over 34%.

Source: DealStats

What is the outlook for second half of 2024?

The positive trend in valuation multiples could be the start of sustained momentum in the M&A market. As economic conditions improve, we expect to see valuations and deal activity return to pre COVID-19 levels. Additionally, private equity firms are beginning to offload portfolio company assets that have been in the queue well past the typical five-year holding period due to recent economic volatility. Lastly, private equity firms are still sitting on roughly $2.7 trillion in dry powder which should provide plenty of fuel to keep the flywheel humming. What could possibly circumvent the improvement in the market? Well, the last piece of the puzzle might unfold in the November Presidential Election.