Concerned about the M&A environment? Look at our top three considerations.

One – Deal Flow

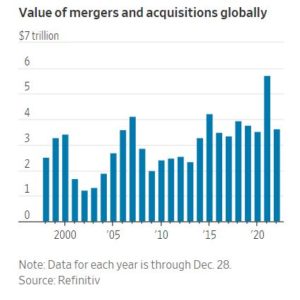

According to a recent Wall Street Journal article, the total value of M&A deals on a global basis fell 37% in 2022 from the record high established in 2021, as depicted in the below chart:

Two observations: First, these numbers are global and are primarily composed of large company transactions vs. smaller, privately owned companies. Second, note that while 2022 represented a significant drop-off from the peak in 2021, as reflected above, 2022 results were still one of the higher totals over the last 20 years.

Additionally, a recent Reuters article outlined that private equity investments slumped by 35% during the calendar year 2022. For 2023 however, this will be offset by the significant overhang of available capital (“dry powder”) that according to Pitchbook stood at $1.2 Trillion at the end of Q3 2022.

Conclusion:

Yes, deal flow will fall from its high point in 2022, but small company deal flow should strengthen in Q2 2023 and will stay on par to prior period transaction levels – there is simply too much capital that needs to be placed at the private company level.

Two – Economics

The picture here is clearer – and clearly it is not very appealing. Interest rates are at their highest level in over fifteen years with the benchmark overnight borrowing rate at 4.5%. The consensus is 2023 should see additional increases up to 5% with no prospective reductions until 2024 (assuming inflation begins to soften). As for inflation, at the end of November 2022, inflation stood at 7.2% for the Consumer Price Index from the period November 2021 (down from 9.1% at mid-year 2022). Given a target inflation rate of 2% annually, inflationary pressure should remain through 2023 if not beyond.

Conclusion:

The economic environment will prove to be a headwind for private business M&A in 2023. The common rule of thumb is deal prices should move opposite (marginally) to the respective move in interest rates as an indicator of the cost of money. With higher financing costs in combination with the threat of a real or perceived recession in 2023, small business sellers should anticipate a softer market from the prior year highs in 2022. But, as outlined in the first point under Deal Flow, continued demand for profitable private companies should keep prices close to the most recent three-year average.

Three – Valuations

While closely tied to the economic factors set forth above, valuation attributions are specific to the size and segment of the offering. On the one hand, a recent Reuters article outlined a Q4 2022 contraction of 56% to $641.2 Billion in the global M&A market; whereas, on the other hand, the Deal Stats Value Index for 4Q 2022 (this publication is more indicative to the smaller business M&A marketplace), posted average increases in both EBITDA and revenue multiples in Q3 2022 from Q2 2022 when factoring in all the business segments. Overall, the smaller business market continues to be a Seller’s market, but relative to the economic backdrop, Buyer’s will be highly selective, and valuations should reflect that.

Overall Conclusion:

For the small business M&A market in 2023, most valuations will fall from the needle peeks in 2022; however, depending upon the individual offering factors such as: business segment, profitability and revenues, combined with the underlying demand for private companies in general, we believe valuations will remain historically competitive to the average of the most recent years. Said another way, despite a challenging economy, and the significant jump in interest rates, we believe well managed, profitable small companies should be well positioned and find ample interest in 2023.